Why Your Homeowners Insurance in New York Is Ballooning in 2025? And What Smart Homeowners Are Doing to Fight Back

If you're a homeowner in New York, you may have felt a sting from rising insurance premiums lately. Between climate change, material costs, regulatory pressures, and shifting insurer strategies, the landscape is changing fast. But knowing what’s driving the increases — and how to respond — can help you protect your home without overpaying. Read on for today’s biggest trends and what exactly you should do.

What’s Fueling the Rise in Homeowners Insurance Costs in New York?

Here are the most important forces pushing your rates up — with current data and NY‐specific insights:

Severe Weather & Climate Risks Are Increasing Losses

Storm frequency, flooding, winter freeze damage, and coastal risks are all more severe in New York. NOAA and state climate data show that repair costs are rising. This increase is due to various factors, including flooding, hurricane damage, frozen pipes, and ice dams. Homes in flood-prone or coastal zones see much higher risk exposure.

Lawmakers are investigating New York’s property insurance market due to climate-driven disasters plus affordability concerns.

Material & Labor Inflation

The cost to repair or rebuild after damage has risen sharply. This increase is due to higher prices for lumber, metals, roofing materials, and skilled labor. These costs feed directly into what insurers must pay out, which in turn raises premiums.

Regulatory & Market Pressures

Insurers are becoming stricter with underwriting. They are raising deductibles or even pulling out of high-risk ZIP Codes. This is especially true for areas at risk of floods or hurricanes.

New York homeowners are also dealing with affordability issues and pressure on state/regulators to scrutinize insurance premium hikes.

Credit Score, Claims History & Location Are Bigger Drivers Than Ever

Homeowners with lower credit scores pay substantially more. Recent data from New York indicates that homeowners with excellent credit typically pay approximately $1,060 annually. This figure pertains to specific coverage levels. In contrast, those with poor credit could face premiums exceeding $2,400 for similar coverage.

If you've filed prior claims, rates tend to jump steeply. Moving within New York City vs Upstate also has big risk-based differences.

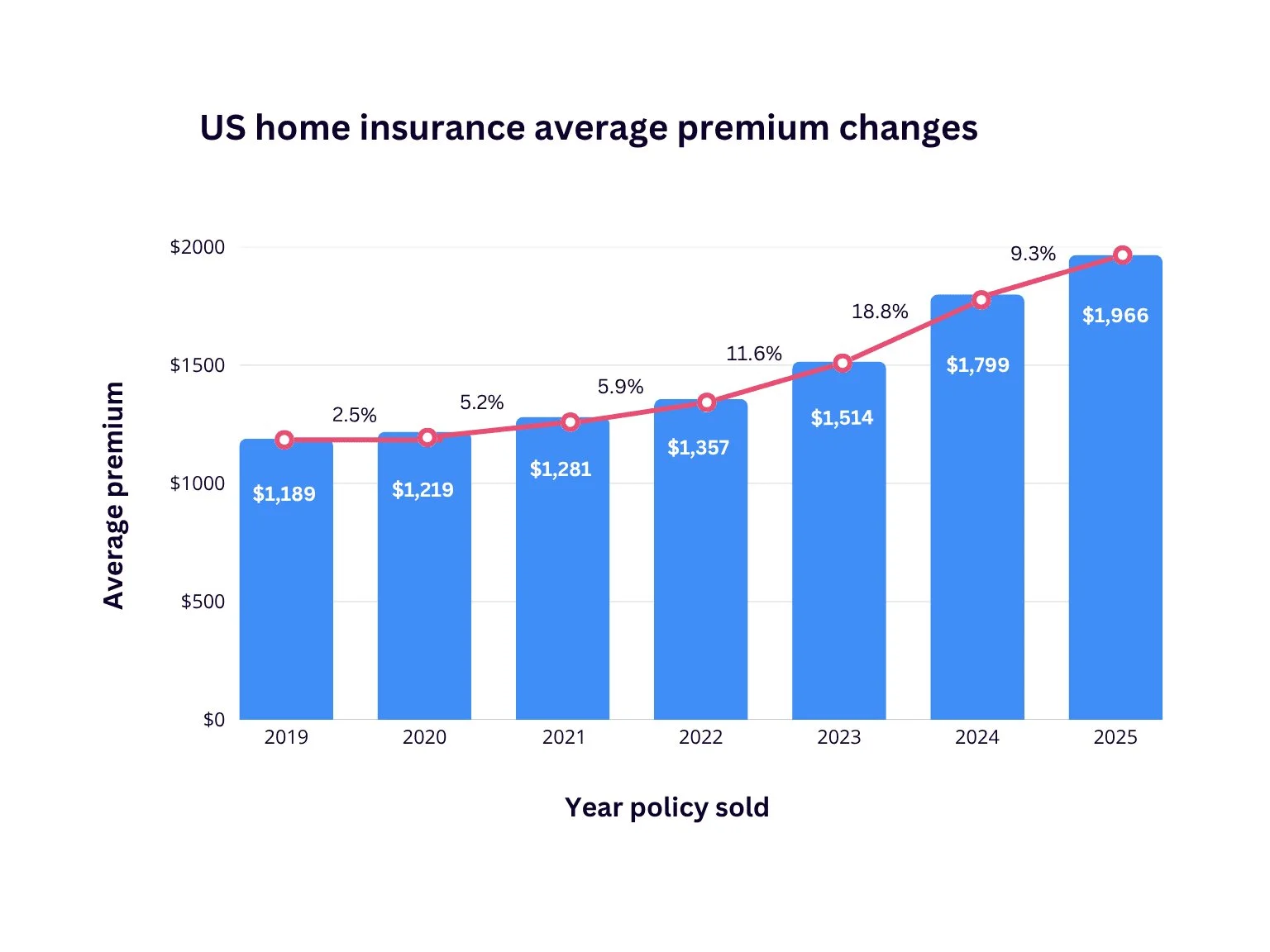

National Trends Amplify Local Pain

Homeowners' insurance premiums in the U.S. have risen sharply. They have increased by 74% over the past 20 years. In contrast, home prices have only gone up by about 40% when adjusted for inflation.

Insurers are raising rates by about 8%+ in many areas for 2025, above inflation, to cover increasing losses.

What It’s Actually Costing NY Homeowners?

Premiums for New York homeowners are climbing faster than the national average. Here’s a breakdown of what people are actually paying in 2025:

| Factor | Average Annual Premium |

|---|---|

| New York State Average | $1,229 |

| NYC Metro Area | $1,700 – $1,800 |

| Excellent Credit Score | $1,060 |

| Poor Credit Score | $2,400+ |

| High-Risk Coastal Zone | $2,000 – $2,500+ |

Key Takeaway: Depending on where you live and your financial profile, New York homeowners could be paying nearly double the national average. Reviewing your coverage and exploring discounts can make a significant difference in 2025.

What Smart NY Homeowners Are Doing to Manage Costs?

Raising deductibles or switching to policies with higher out-of-pocket costs for certain perils.

Bundling home with auto insurance to get multi-policy discounts.

Installing protective devices (storm shutters, updated roofs, freeze protection) to reduce risk and qualify for discounts.

Moving out of flood risk map zones when possible, or getting flood insurance separately.

Shopping around each year, switching carriers when better deals are available.

Making sure the credit score is in good shape and the claims history is clean.

Key Takeaways: Your Action Plan to Fight Rising Insurance Premiums

Audit Your Coverage Annually

Don’t assume your current policy is still the best deal. Scope, location, and risk factors may have changed.Mitigate Local Risks Directly

If you’re in a flood zone or snowy region, invest in upgrades (good roofing, proper sealants, snow guards, water sensors). Small improvements can lower premiums materially.Use Discounts Aggressively

From bundling to protective devices to loyalty, many discounts are under-leveraged in NY.Improve Your Credit & Claim History

Even a small improvement in your credit score or remaining claim-free for a few years can lower your premiums by hundreds each year.Plan for Non-Standard Coverage Needs

Flood, earthquake, coastal wind, snow load — standard policies don’t always cover these. Budget separately if you need these.

Final Word

Homeowners insurance in New York is not only increasing in cost but also becoming more specific and risk-aware. This trend particularly affects those living in high-hazard areas, making insurance more expensive for them. But being proactive, making smart home improvements, and shopping wisely can give you more control over what you pay.

If you are interested, I can create a localized version for you. This would cover areas like NYC, Long Island, Hudson Valley, and Upstate. It will include premium comparisons by ZIP code, which often attracts significant traffic.

References

“Average Cost of Homeowners Insurance in New York (2025)”, MoneyGeek. MoneyGeek.com

“Home Insurance Trends Report”, The Zebra. The Zebra

“Report: Home Insurance Rates to Rise 8% in 2025”, Insurify. Insurify

“Homeowners Insurance Crisis Continues to Weigh on Homeowners”, Harvard Joint Center for Housing Studies. Harvard Joint Center for Housing Studies

“Rising costs from climate change is driving insurers out of … New York”, City & State NY. City & State New York

“NY Homeowners Insurance: Best Coverage Tips for 2025”, Mitchell Joseph Insurance. Mitchell-Joseph Insurance

“Lawmakers seek to investigate NY’s soaring home …”, Times Union. Times Union