New York Contractor Insurance in 2025: Why Costs Are Exploding & How to Stay Ahead

If you are a contractor in New York, you have likely faced a significant challenge. Insurance premiums are taking a larger share of your profits than ever before. With Labor Law §240 (Scaffold Law) in place, New York faces aggressive lawsuits. Additionally, the costs of materials and labor are rising. As a result, New York is the most expensive state in the U.S. for contractor insurance.

However, there is no need to panic. By understanding the factors involved, you can take strategic actions to achieve your goals. This will help you safeguard your business. Additionally, you can refine your bids. Ultimately, this approach may give you a competitive advantage over those who do not adapt.

Why Contractor Insurance Costs More in New York?

1. Labor Law §240 (Scaffold Law)

NY is the only state with strict liability on gravity-related falls.

Contractors are automatically liable for injuries—even if workers fail to follow safety protocols.

Verdicts and settlements average $4.9M per case—with many topping $10M.

Translation: One accident could sink your business if you’re not properly insured.

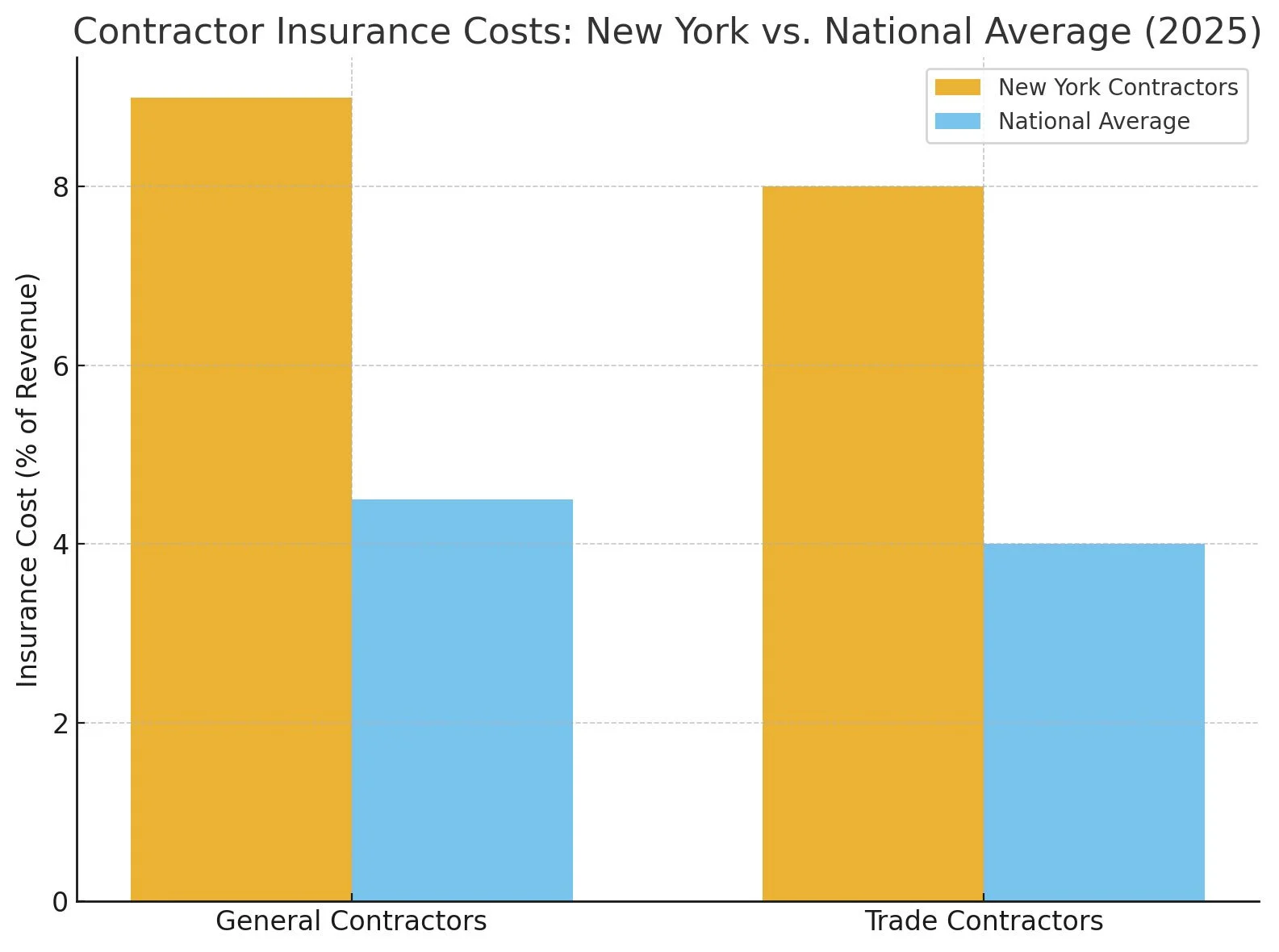

2. Premiums Double the National Average

Contractors in New York spend 7–10% of revenue on insurance.

In most other states, the cost is just 3–5%.

NYC contractors, especially those in high-rise, scaffolding, and demolition, pay the highest rates. In contrast, Upstate firms also pay above national averages.

3. 2025 Rate Increases Across the Board

General Liability: +5–15% (biggest hikes for trades exposed to Scaffold Law).

Commercial Auto: +10–15% (driven by accident severity & inflation).

Workers’ Comp: Flat to +5%, but claims are more expensive due to medical inflation.

Builder’s Risk: Restricted capacity + sublimits in hurricane/NYC flood zones.

4. Limited Carrier Appetite

Many insurers avoid NY contractors altogether.

Those that remain add exclusions, higher deductibles, or force wrap-up programs.

Smaller trades like roofing, masonry, demo, and scaffolding are hardest hit.

What does this mean for you?

Thinner margins → 7–10% of revenue lost to insurance.

Harder bidding → underestimate premiums, and you either lose bids or win jobs at a loss.

Increased legal exposure → one fall could mean millions in liability.

Cash flow strain → higher deductibles and slower certs delay projects.

How NY Contractors Can Take Control?

New York contractors face higher insurance costs than the national average. But with the right strategies, you can reduce premiums and strengthen your business. Here’s how:

| Strategy | What To Do? | Why It Works? |

|---|---|---|

| Elevate Safety | Document scaffold checks, run toolbox talks, enforce PPE, and keep inspection logs. | Reduces claims and positions your business for better premiums. |

| Vet Subcontractors | Require GL & Workers’ Comp, verify COIs, and add your business as additional insured. | Shifts exposure and limits liability from subcontractor mistakes. |

| Use a NY Specialist Broker | Work with a broker who understands NY construction law and specialty markets. | Ensures coverage is tailored and avoids costly exclusions. |

| Smart Policy Design | Consider higher deductibles, umbrella layers, and strategic bundling. | Balances affordability with protection while avoiding overlap. |

| Annual Market Check | Shop the market yearly, audit loss runs, and correct coding errors. | Even small savings compound over time, improving profitability. |

| Monitor Reform Efforts | Stay updated on Scaffold Law/Labor Law reform and adjust policies quickly. | Keeps you ahead of regulatory shifts that affect liability. |

Key Takeaway: With safety documentation, smart subcontractor vetting, and a knowledgeable broker, New York contractors can cut insurance costs and gain leverage in a tough market.

2025 Premium Increases by Coverage Type

Insurance premiums for New York contractors are climbing faster than the national average. Here’s how the increases compare by coverage type in 2025:

| Coverage Type | New York Increase (2025) | National Average (2025) |

|---|---|---|

| General Liability | +12% | +6% |

| Commercial Auto | +8% | +4% |

| Workers’ Compensation | +10% | +5% |

| Builder’s Risk | +15% | +7% |

Key Takeaway: New York contractors are paying nearly double the national rate in premium increases for 2025. Strategic risk management and the right broker can make a measurable difference.

Localized Insight: NYC vs. Upstate NY

NYC Contractors → Face the steepest premiums due to high-rise work, union labor, and dense litigation environment.

Upstate Contractors → They tend to charge more than the national averages. However, they often offer better rates if projects do not require scaffolding or heavy demolition.

Statewide Trend → Carriers are retreating, so contractors in all regions need to document safety and seek specialized brokers.

Final Word

New York contractors are under enormous pressure in 2025. Insurance isn’t just a line item—it’s a competitive advantage if managed right. Firms that prioritize safety can work with the right brokers. They can also design their policies effectively. This approach allows them to bid with confidence. It helps protect their employees and supports profitable growth.

Don’t let insurance costs control your business—take control of your insurance strategy.

Ready to explore tailored contractor insurance in New York? Contact Blue Rock Insurance Services today to protect your projects and strengthen your bids.