Understanding General vs. Professional Liability Insurance

Navigating the world of business insurance can be daunting. Two key types are general and professional liability insurance. Understanding their differences is crucial for business owners and professionals alike.

General liability insurance covers third-party bodily injury, property damage, and advertising injury. It's essential for businesses with physical locations or those interacting with the public.

Professional liability insurance, often called errors and omissions insurance, protects against negligence and mistakes in professional services. It's vital for service-based businesses and professionals offering expert advice.

Choosing the right insurance can protect against lawsuits and financial losses. This guide will help you understand these insurance types and make informed decisions for your business.

What Is General Liability Insurance?

General liability insurance is a protective shield for businesses. It covers a broad range of risks that might occur. This type of insurance is crucial for any business dealing with the public.

Its primary purpose is to protect businesses from third-party claims. These claims could involve bodily injury, property damage, or even advertising injury.

A claim might arise if someone gets hurt on your business property. In that case, general liability insurance could cover medical expenses. It offers peace of mind to business owners worried about unexpected events.

General liability insurance is often required by landlords or clients. It is commonly recognized as a part of a comprehensive business insurance package. Businesses with high foot traffic find this insurance particularly valuable.

Here are typical coverages included in general liability insurance:

Bodily injury and property damage

Medical payments

Legal defense costs

Personal and advertising injury

Overall, it's an essential foundation for most businesses. It safeguards against significant financial setbacks from potential claims.

What Is Professional Liability Insurance?

Professional liability insurance is tailored for service-oriented businesses. It shields you from claims of errors or negligence in your professional services. This type of insurance is also known as errors and omissions insurance.

Unlike general liability, this policy focuses on professional mistakes. It's crucial for professions that offer advice or services. This includes consultants, architects, and healthcare providers.

If a client suffers a financial loss due to your service, a claim might arise. Professional liability insurance covers legal fees and settlements in such cases. It ensures you won't face severe financial strain from lawsuits.

This insurance is often a requirement for client contracts. It's particularly important in fields where expertise and precision are vital. Firms that depend heavily on client trust find it indispensable.

Typical coverages under professional liability insurance include:

Legal defense costs

Settlements and judgments

Claims of misrepresentation

Breach of contract

Overall, professional liability insurance is crucial for maintaining your business's reputation. It's an essential layer of protection for any professional service provider. It helps manage risks unique to your profession.

Key Differences Between General and Professional Liability Insurance

Understanding the core differences between general and professional liability insurance is crucial. Each serves distinct purposes in risk management. Below, we explore these differences in more detail.

General liability insurance is broader in scope. It covers bodily injury, property damage, and advertising injury. It's vital for businesses with physical presence and public interactions.

Professional liability insurance is more specialized. It caters specifically to service errors or omissions. Professions like consulting or healthcare often require this insurance.

A key difference lies in the nature of coverage. General liability covers physical risks, like slip-and-fall accidents. In contrast, professional liability covers non-physical risks, such as negligence.

The requirements for each type also differ significantly. General liability is often required by landlords and clients. This makes it foundational for businesses of all sizes.

In contrast, professional liability tends to be required by client contracts. This is especially common for service-based professions. Industries with high client interaction often mandate this insurance.

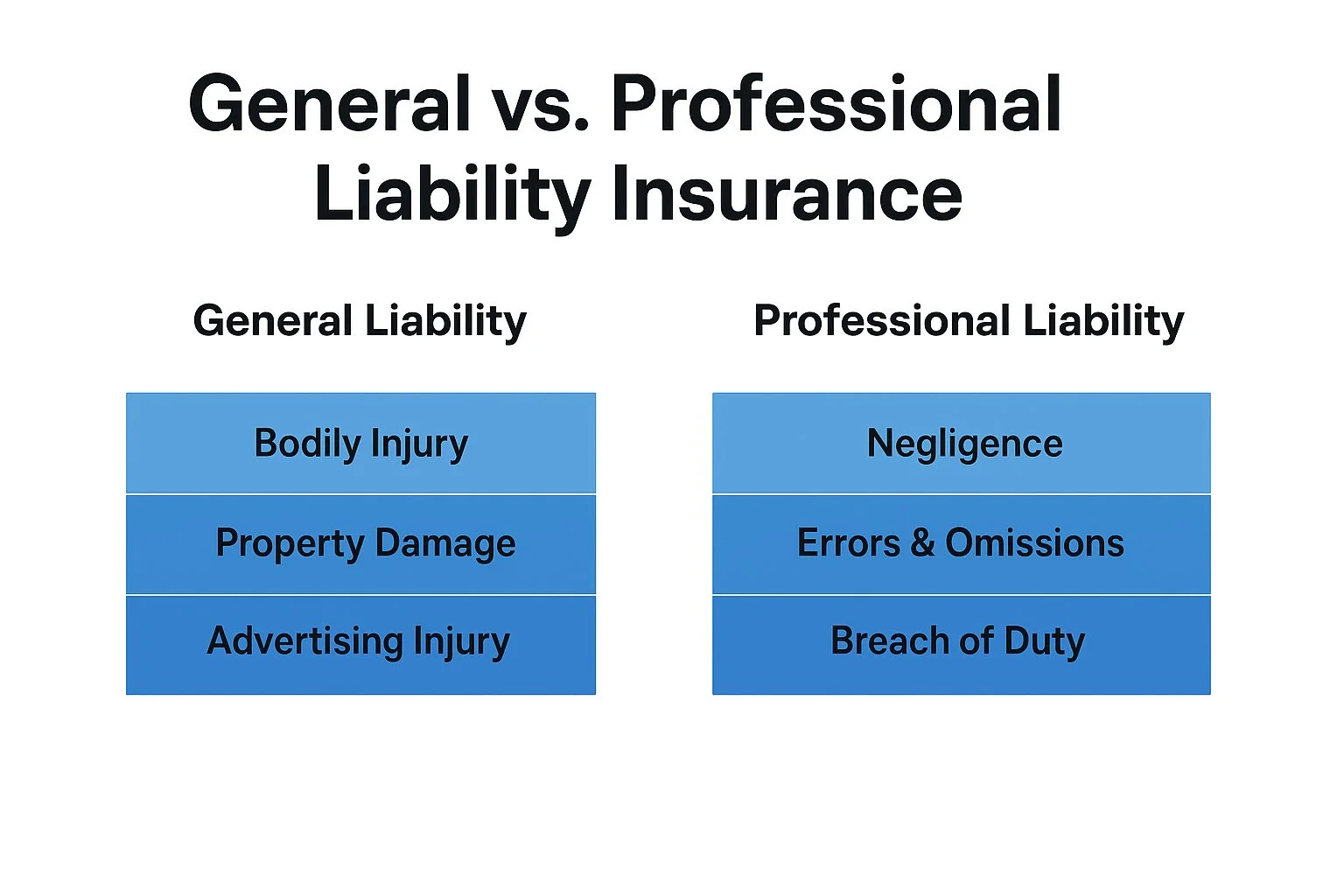

General Liability Insurance Covers:

Bodily Injury

Property Damage

Advertising Injury

Professional Liability Insurance Covers:

Errors and Omissions

Legal Defense for Negligence

Breach of Duty

Ultimately, both insurances serve to protect against financial losses. Yet, they target different aspects of business operations. Selecting the right type—or both—depends on the specific needs of your business. Recognizing these differences aids in crafting a comprehensive insurance plan.

Who Needs General Liability Insurance?

Businesses interacting with the public often need general liability insurance. It offers protection against a variety of common risks. Companies with brick-and-mortar locations particularly benefit from this coverage.

From small shops to large retail chains, any business with physical premises should consider it. If your business involves client visits or public events, this insurance is essential. It safeguards against accidents and unforeseen incidents.

Even businesses that operate online can benefit. Those who manufacture or distribute products may face product liability issues. Hence, general liability insurance is valuable for any business seeking comprehensive risk management.

Businesses That Need General Liability Insurance:

Physical stores and offices

Companies hosting public events

Online businesses with physical products

Who Needs Professional Liability Insurance?

Professional liability insurance is crucial for service-oriented businesses. It's also known as errors and omissions coverage. Professionals providing specialized advice or services should consider it.

Consultants, architects, and healthcare providers benefit greatly. Mistakes or omissions in their work can lead to costly claims. This insurance helps protect their reputation and finances.

Freelancers and small business owners providing expert advice also need it. It covers liabilities that general insurance doesn't. Knowing when you're covered brings peace of mind.

Even tech professionals can be at risk. Software errors or advice leading to client losses might result in claims.

Professionals Who Benefit From This Insurance:

Consultants and advisors

Healthcare professionals

Architects and engineers

IT and tech professionals

General Liability vs. Professional Liability: Real-World Examples

Understanding the difference between general and professional liability insurance is clearer with examples. Real-world scenarios often highlight their distinct roles.

Imagine a restaurant owner facing a slip-and-fall incident. The customer gets injured on the premises. Here, general liability insurance kicks in to cover medical expenses and related claims.

On the other hand, consider a consultant providing incorrect advice. The error results in financial loss for a client. Professional liability insurance covers such negligence claims.

Similarly, think about an architect making a design mistake. This leads to project delays and extra costs. Professional liability insurance would be crucial in this case.

Yet, if the architect's office experienced a fire causing property damage, general liability would cover the physical losses.

Real-World Scenarios Illustrating Coverage:

Restaurant slip-and-fall: General liability

Consultant's advice error: Professional liability

Architect's design mistake: Professional liability

Office fire damage: General liability

Cost Factors: General vs. Professional Liability Insurance

The cost of liability insurance can vary greatly depending on several factors. Understanding these elements can aid in budgeting and selection.

General liability insurance premiums depend on the business size and industry. For instance, a large retailer might pay more than a small café due to higher risk exposure.

Location is another key factor. Businesses in areas with higher claims tend to incur higher premiums.

Professional liability insurance costs hinge on the profession and perceived risk. A healthcare provider may face higher premiums than a graphic designer due to potential liabilities.

Coverage limits also influence premiums for both insurance types. Higher coverage usually means higher costs.

Key Cost Factors Include:

Business size and industry

Location of operation

Profession and risk level

Desired coverage limits

Understanding these factors helps in selecting suitable and affordable coverage for your business needs.

General vs. Professional Liability Insurance

Both general and professional liability insurance protect your business, but they cover different risks. Here’s a clear comparison to help you understand why each type matters:

| Coverage Type | Why You Need It |

|---|---|

| General Liability | Covers bodily injury, property damage, and advertising injury. Essential for businesses with physical locations or those interacting with the public. |

| Professional Liability | Protects against errors, omissions, or negligence in professional services. Vital for service-based businesses and professionals providing expert advice. |

| Example Claim | General liability: a customer slips and falls in your store. Professional liability: a consultant gives incorrect advice causing financial loss. |

| Requirement | General liability is often required by landlords or clients. Professional liability is frequently required in client contracts for service-based professions. |

| Who Needs It | General liability: physical stores, public events, product distributors. Professional liability: consultants, architects, healthcare providers, IT professionals. |

Key Takeaway: General liability covers physical risks, while professional liability protects against errors and negligence. Many businesses benefit from carrying both types to ensure full protection.

Do You Need Both Types of Insurance?

Determining if your business needs both general and professional liability insurance is crucial. Each type addresses different risks, providing unique protections.

For businesses with physical locations, general liability is essential. It protects against common hazards like slips, falls, or property damage.

Service-based businesses benefit significantly from professional liability coverage. This insurance defends against claims of negligence or errors in professional advice.

Many businesses find a combination of both policies beneficial. This ensures comprehensive protection against a wide range of potential liabilities.

Considerations for Needing Both Insurance Types:

Operating a physical business location

Providing expert advice or services

Facing various liability risks

Choosing both may offer peace of mind, safeguarding your business from diverse challenges.

How to Choose the Right Liability Insurance for Your Business

Selecting the right liability insurance involves understanding your specific business needs. A thorough risk assessment can guide your decision.

Consider the nature of your operations and the potential risks involved. For physical operations, general liability insurance is often a necessity.

For businesses offering specialized services, professional liability insurance may be critical. Assess the frequency and impact of client interactions in your field.

Consult with insurance professionals to gain insights tailored to your industry. Their expertise can help ensure adequate coverage.

Factors to Evaluate:

Business type and industry

Risk exposure and history

Client expectations and contracts

Ultimately, informed decisions on liability insurance can safeguard financial stability and business integrity. Choose wisely to match your company's distinct needs.

Frequently Asked Questions About Liability Insurance

Many business owners are unsure about the distinctions between different liability insurances. Clarifying these differences is essential for making the right choice.

One common question is whether professional liability is the same as general liability. They serve different purposes and cover different risks.

Business owners often ask if both insurances are necessary. For some, both policies are essential for comprehensive protection.

Key Questions:

What does each policy cover?

Are both insurance policies required for my business?

How do I determine the right coverage limits?

Asking these questions helps identify the most suitable coverage for safeguarding your business effectively. Understanding your options ensures informed decisions.

Protecting Your Business with the Right Coverage

Selecting the right insurance is key to protecting your business. It shields against unforeseen risks and potential financial losses.

Understanding the difference between general and professional liability insurance can simplify this task. It helps tailor coverage to your specific needs.

By choosing the right policies, you ensure comprehensive coverage. This not only protects your assets but also contributes to your business's sustainable growth and stability. Always review your coverage regularly as your business evolves.