What Insurance Does a Restaurant Need in NYC?

New York City's restaurant scene is a vibrant tapestry of culture and flavor, a dream destination for culinary entrepreneurs. Yet, behind the warm atmosphere and the scent of delicious dishes lies a complex web of risks. These challenges can test even the most experienced restaurateur. For establishments such as Khaosan, a Thai restaurant in Brooklyn, the management of risks is essential. This responsibility falls to Amita, the owner. It is a crucial aspect of her daily operations that contributes to the restaurant's success.

Running a restaurant here involves managing various revenue sources. These include dine-in, online orders, in-house delivery, and catering. Additionally, restaurants often take part in notable events like the Thai Select festival and Pig Week on Staten Island. Each of these activities introduces unique vulnerabilities, from equipment failures and inventory spoilage to liability claims and payment disputes.

Having the right insurance coverage is not merely a regulatory requirement; it is a strategic asset. This coverage enables restaurant owners to focus on growth and creativity. They can do so with confidence, knowing their business is protected from unforeseen challenges. Below, we will examine the insurance policies that every restaurant in New York City should consider. To illustrate these points, we will use the example of a real-world establishment, Khaosan.

An Inside Look: Customizing Insurance for Your NYC Restaurant

To provide new restaurant owners with a clear understanding of the insurance process, we spoke with Amita. She is the owner of the well-known Khaosan Thai restaurant in Brooklyn. This conversation illustrates how a good insurance review should go.

Blue Rock: Amita, thanks for your time. Business seems to be booming! To start, can you walk me through a typical week at Khaosan? It helps us understand your unique risk profile.

Amita: Of course! It’s always busy, which is a good problem to have. We’re packed for lunch and dinner, of course. But it’s not just dine-in. Our online orders are a huge part of the business now. We also handle our own local deliveries with a couple of staff members. We are becoming more involved in catering for major food events. Last month, we participated in the Thai Select festival.

Blue Rock: That’s a fantastic mix of revenue streams. It also means your insurance needs to be more comprehensive than a standard policy. Let's dig into that. What’s your single biggest worry when you lock up at night?

Amita: Honestly? The walk-in freezer breaking down. We import so many specific ingredients directly from Thailand. If we lost it all, it wouldn’t just be the cost of the food—it would mean we’d have to take items off the menu until we could restock. I’ve heard nightmares about that from other owners.

Blue Rock: That’s one of the most common and devastating risks. The good news is, that’s exactly what Equipment Breakdown and Spoilage Coverage is for. It is an add-on that will pay for the compressor repair and reimburse you for the full value of the lost inventory. It turns a catastrophe into a manageable incident.

Amita: That’s a relief to hear. Another thing—my bartenders create amazing signature cocktails, but it makes me nervous. What if someone has too much to drink and something happens after they leave?

Blue Rock: That’s a very sharp instinct. New York has strict "Dram Shop" laws. Your standard liability policy likely excludes this exposure. You need a separate Liquor Liability Policy. It protects you specifically from lawsuits arising from the service of alcohol. For a restaurant with a bar program as popular as yours, it’s not optional; it’s essential.

Amita: Okay, that makes sense. What about my delivery? My servers use their own cars to drop off orders. Are we covered if they get into an accident?

Blue Rock: That’s a critical question. The answer is no—their personal auto policies will not cover an accident that happens while they are working for you. This is one of the biggest gaps for restaurants. You need Hired and Non-Owned Auto (HNOA) Insurance. It protects Khaosan from the liability if your employee is at fault in an accident while delivering an order.

Amita: I had no idea. I’m glad we’re talking about this. One more issue: we get credit card chargebacks every few months. Customers disputing charges, sometimes falsely. It’s frustrating and costs us money. Is there anything that can help with that?

Blue Rock: Absolutely. This is a growing problem that many owners don’t think of as insurable. Many Cyber Liability Insurance policies now include coverage for “payment card disputes” or “cyber fraud.” It can help cover the costs and lost revenue from fighting those fraudulent chargebacks.

Blue Rock: Finally, with you doing off-site events like Pig Week, we need to ensure your General Liability policy has a endorsement that specifically extends coverage to catering and special events. This way, you’re protected whether someone slips and falls in your dining room or at your festival booth.

Amita: This has been incredibly helpful. It feels less like buying a generic product and more like building a custom safety net for my business.

Blue Rock: That’s exactly the goal. Insurance for a restaurant like yours isn’t one-size-fits-all. It is essential to understand every aspect of your operation. This includes dine-in, delivery, events, and the bar. Each element must be safeguarded effectively.Let’s build that comprehensive plan for Khaosan.

Understanding New York Restaurant Insurance Needs

This guide outlines the main types of restaurant insurance and risk management strategies.

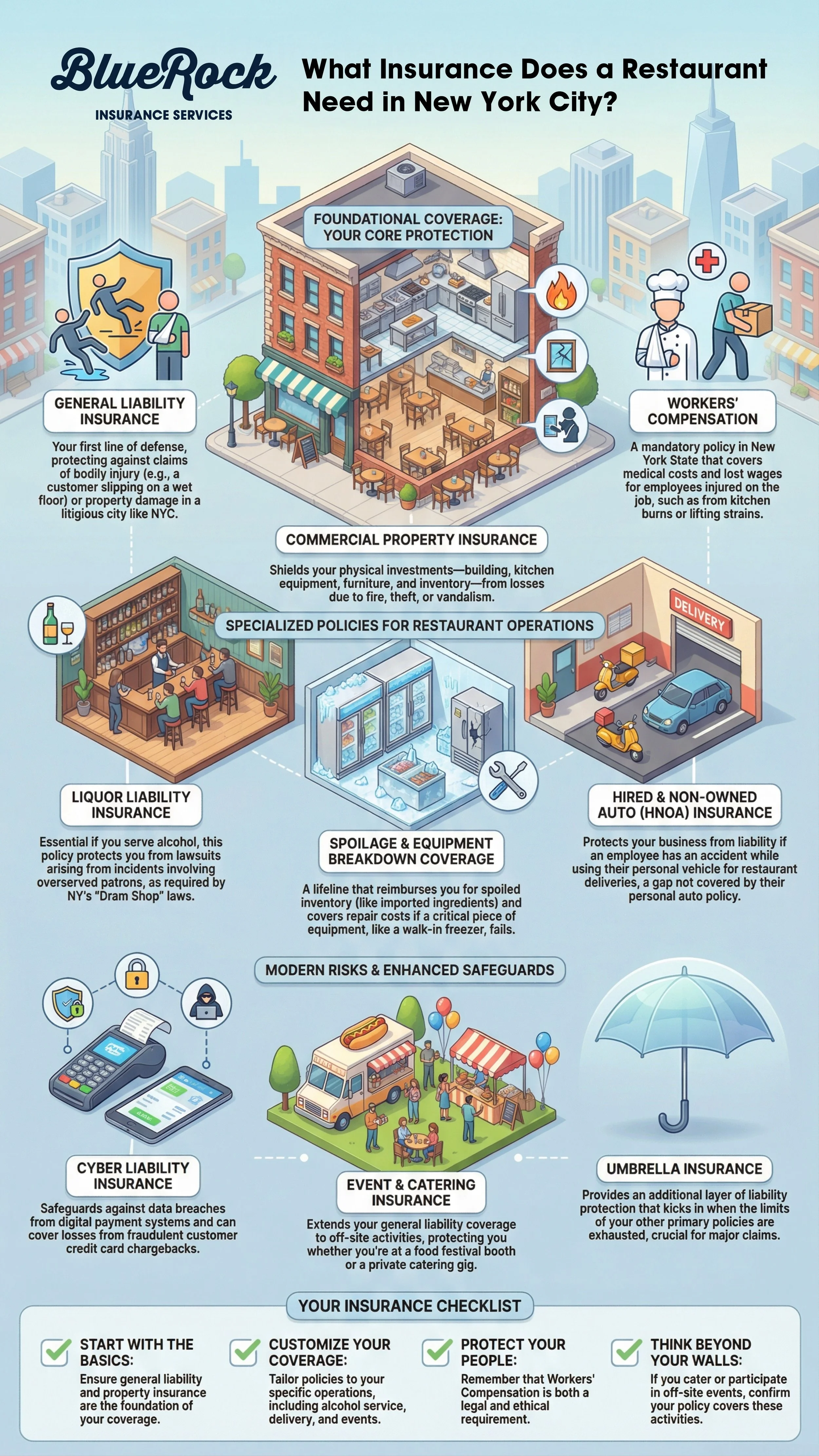

Commercial Property Insurance: Shielding Your Physical Investment

Your restaurant’s space, kitchen equipment, furniture, and inventory represent a significant financial commitment. Commercial property insurance covers losses from fire, theft, vandalism, or certain natural disasters. For Amita, this means that the elegant décor of Khaosan and its specialized kitchen tools are protected. This ensures that one incident does not disrupt operations.

General Liability Insurance: Your First Line of Defense

In a city as litigious as New York, general liability insurance is non-negotiable. It protects against claims of bodily injury (e.g., a customer slipping on a wet floor) or property damage. Given the bustling nature of restaurants like Khaosan, this coverage is indispensable for mitigating legal and medical costs.

Liquor Liability Insurance: A Must-Have for Serving Alcohol

If your restaurant serves cocktails, wine, or beer, liquor liability insurance is critical. New York’s "Dram Shop" laws hold establishments accountable for incidents involving overserved patrons. For Khaosan, which is famous for its Thai-inspired cocktails, this policy provides essential protection. It safeguards the establishment against claims arising from alcohol-related accidents.

Workers’ Compensation: Protecting Your Team

New York State mandates workers’ compensation insurance for businesses with employees. It covers medical costs and lost wages for employees injured at work. This includes injuries like kitchen burns or strains from lifting. For Amita and her team of 20, this policy ensures that both staff and business are protected.

Commercial Auto or Hired/Non-Owned Auto Insurance

If your restaurant offers delivery, it is important to have the right insurance. This applies whether you use your own vehicles or your employees' cars. You should consider getting commercial auto insurance or hired/non-owned auto (HNOA) insurance. Personal auto policies typically exclude accidents occurring during commercial activities. For Khaosan, which handles its own deliveries, HNOA coverage mitigates the risks associated with transportation.

Spoilage and Equipment Breakdown Coverage

Equipment failures can lead to significant financial losses, especially when they result in spoiled inventory. Spoilage coverage reimburses for lost perishables, while equipment breakdown coverage addresses repair or replacement costs. For a restaurant like Khaosan, which relies on specialized equipment and fresh ingredients, these policies are a lifeline.

Cyber Liability Insurance

With the rise of online orders and digital payment systems, cyber liability insurance has become increasingly important. It safeguards against data breaches and can also cover losses from fraudulent chargebacks. This is a common issue for restaurants dealing with dishonest disputes.

Event and Catering Insurance

Participating in off-site events like the Thai Select festival or Pig Week introduces additional liabilities. Event insurance extends your general liability coverage to these occasions, protecting your business when operating outside its usual premises.

Umbrella Insurance: Extra Protection When You Need It Most

Umbrella insurance provides an additional layer of liability coverage beyond the limits of your primary policies. For a growing restaurant like Khaosan, this extra cushion can be invaluable in the event of a major claim.

Key Takeaways for NYC Restaurant Owners

Start with the basics: General liability and property insurance are foundational.

Customize your coverage: Tailor policies to your specific operations, such as delivery, alcohol service, or events.

Protect your people: Workers’ compensation is legally required and ethically essential.

Plan for the unexpected: Spoilage, equipment breakdown, and cyber risks can disrupt even the best-run establishments.

Think beyond your walls: If you cater or participate in events, ensure your policy covers off-premise activities.

For restaurant owners like Amita, insurance is not just a compliance requirement; it is a strategic asset. By recognizing and managing the unique risks of the industry, you can safeguard your investment. This approach also empowers your team and allows you to keep sharing your culinary passion with the world.